Hey everyone,

Most of my content has predominantly been geared towards self-publishing on Amazon KDP. However, I also have a keen interest in investing, and most of the money I make is funneled back into investments.

I didn’t restrict my website or YouTube to being exclusively about KDP, because I wanted the freedom to discuss money in a broader sense. Now that I have reached what I consider financial freedom (which, of course, can mean different things to different people), I am keen on sharing both my financial independence journey along with my KDP experiences. I hope that it can be of value to some of you.

Testing the Waters with Premium Bonds

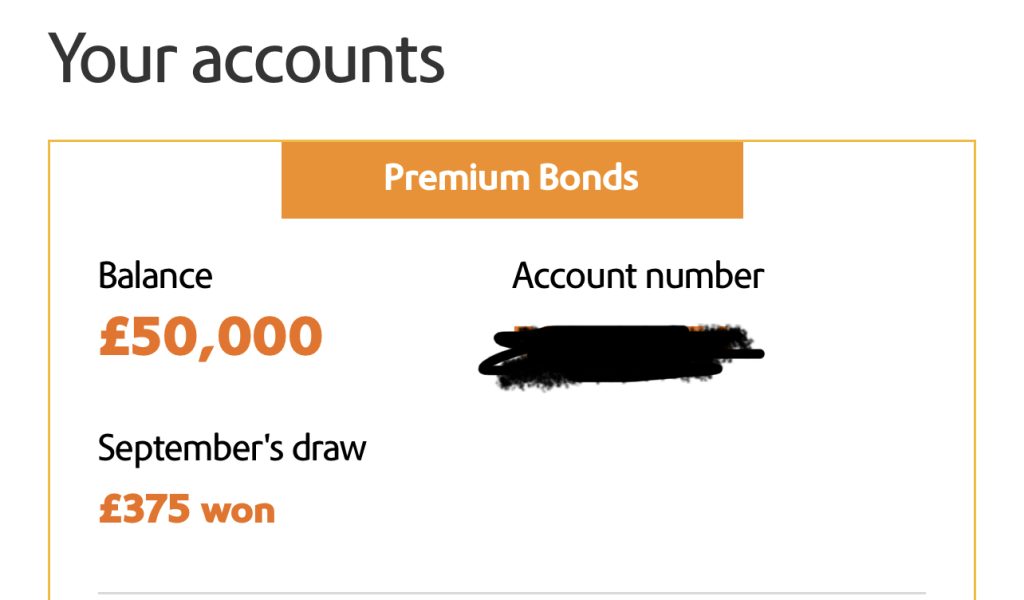

So here I am, testing the waters with one of my latest investments – premium bonds, a concept available in the United Kingdom. In case you aren’t familiar with it, premium bonds are lottery bonds sold by a UK government agency. They don’t offer regular interest or dividends like traditional savings or investment products; instead, they give you a chance to win tax-free prizes through regular monthly draws. (You can see the amount of prizes available in the image above)

You can buy each bond for £1, owning up to a maximum of 50,000 bonds. Naturally, the more bonds you have, the higher your chances of winning in these draws. Prizes range from £25 to a massive £1 million. At this time, the average return based on “average luck” is about 4.65%.

My First Experience and Why I Chose Premium Bonds

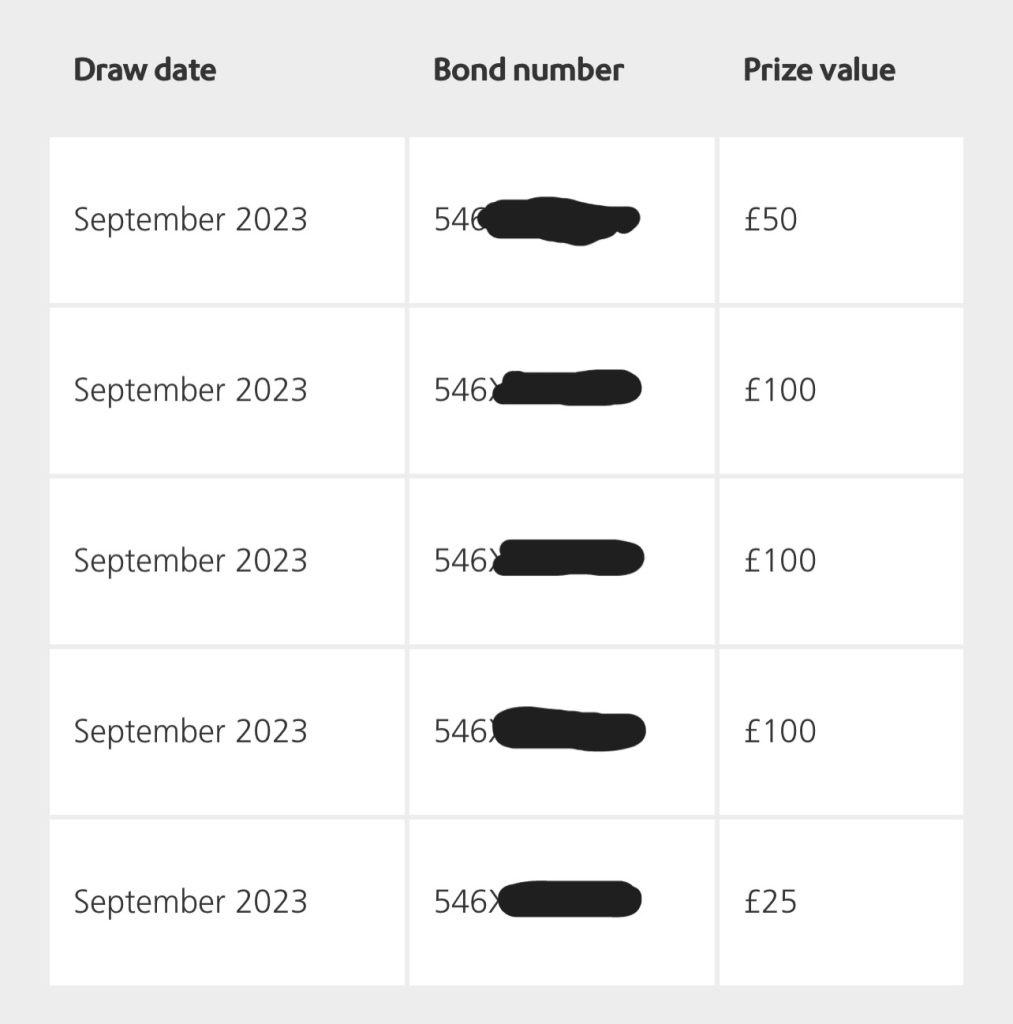

Earlier in September, I received the results of my first prize draw. I own the maximum allowable amount of 50,000 bonds, and I was thrilled to find that I won prizes totalling £375 for the month. This equates to a 9% return on an annual basis, which pleasantly surpassed the average 4.65% return rate. I can’t help but wonder if it was a stroke of beginner’s luck!

Now, why did I choose this unpredictable route of investment instead of just depositing my money into a savings account with a guaranteed 5% return? The answer is well-thought-out: I am in a higher tax bracket, which subjects me to a 40% tax on the interest earned from bank savings. Premium bonds come with a significant advantage here as the prizes are tax-free.

A Thoughtful Decision

To better the actual return of premium bonds, a savings account would need to offer an interest rate of 7.1%, which is quite unlikely given the current rates. Even though the premium bond prizes aren’t guaranteed, the math works out in my favor.

As you can see from the table above, the net return from premium bonds is much better for someone in my position. (LR= lower rate tax payer 20% – HR= higher rate tax payer 40% – AR= Addition rate tax payer 45%)

Building wealth is about making small yet significant decisions that allow me to retain a larger portion of my investments. This strategy enables quicker capital compounding, allowing you to grow your wealth at a faster pace.

While I am aware this post might not resonate with those outside the UK, I hope the underlying principle behind this investment choice offers some food for thought.

I am eager to hear if you would like more content revolving around financial topics. Also, let me know if sharing my monthly premium bond prize draws would be of interest to you.

Take care,

Ben

CHAMP-12/26 SPT-9 BB-18/19 RAIN-1/55/72 CVR- 5/31